The market is off to a rocky start this year, in the last six days, the S&P500 is down nearly -7%, the Russell 2000 -8.5%, and the Nasdaq -8%.

The news of the day again was China and billionaire investor George Soros, who said we might be in a 2008 situation again. But the fact is that the average intra-year decline in the S&P500 in the last 35 years is roughly 14%. Until we breach that mark then this all part of the game.

With today’s near 400 point decline in the Dow Jones, CNBC and Bloomberg both have a “Market in Turmoil” scheduled for tonight.

More importantly, breadth in the short term is getting a little stretched to the downside that might lead to some short-term respite (3-5 days).

Here are the stretched breadth charts:

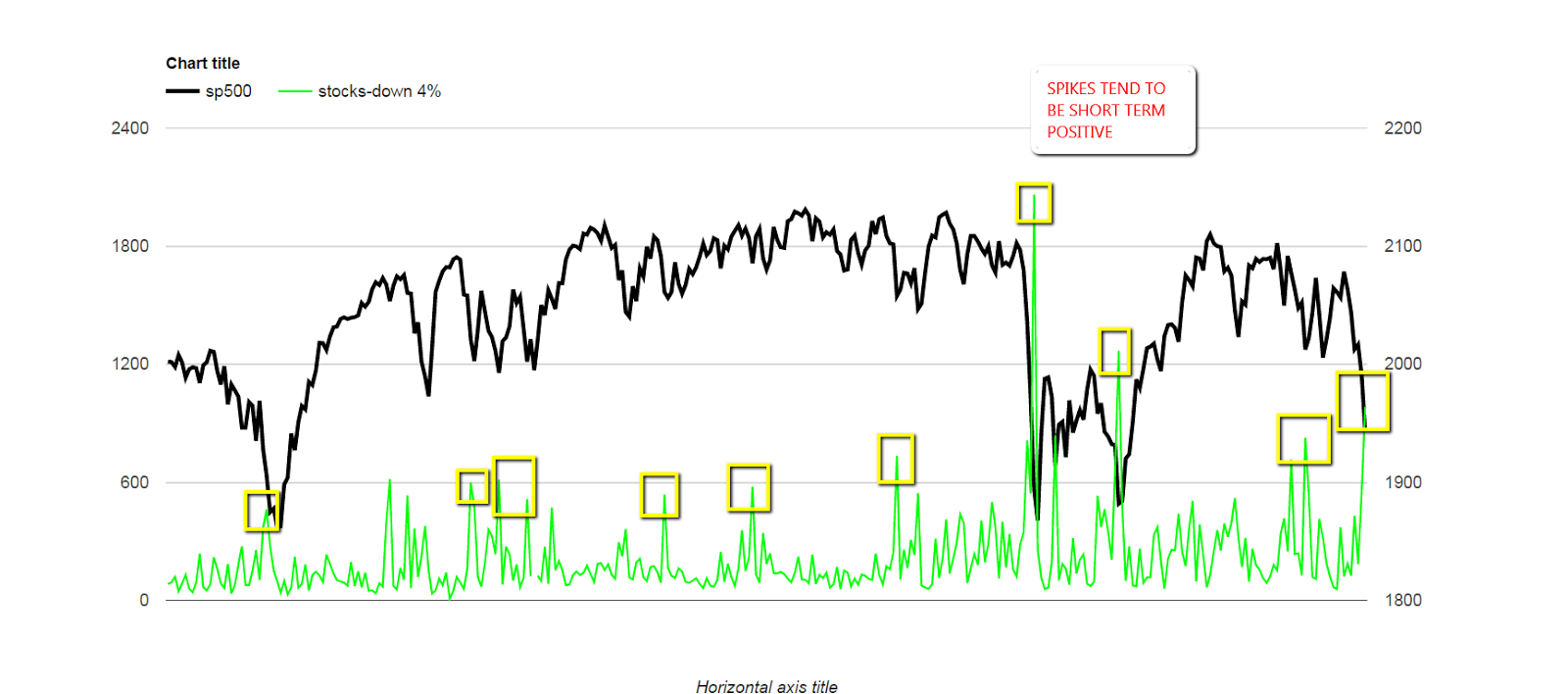

SP500 vs. NYSE, NASDAQ, AMEX, one-day decliners.

We saw a significant spike in stocks down 4% or more today; spikes tend to be short-term positive.

We also saw a large spike today in stocks down 13% or more in the last 34 days; spikes tend to be a short-term positive.

The percent of stocks above their 20-day moving average is also pointing at a dead cat bounce, unless of course we crash, and that rarely happens.

We saw a huge spike in 1 month fresh new lows; again spikes usually mean short-term exhaustion.

The same can be said for 3-month fresh new lows.

The percent of Russell 3000 stocks above their 10-day moving average is also at exhaustion levels.

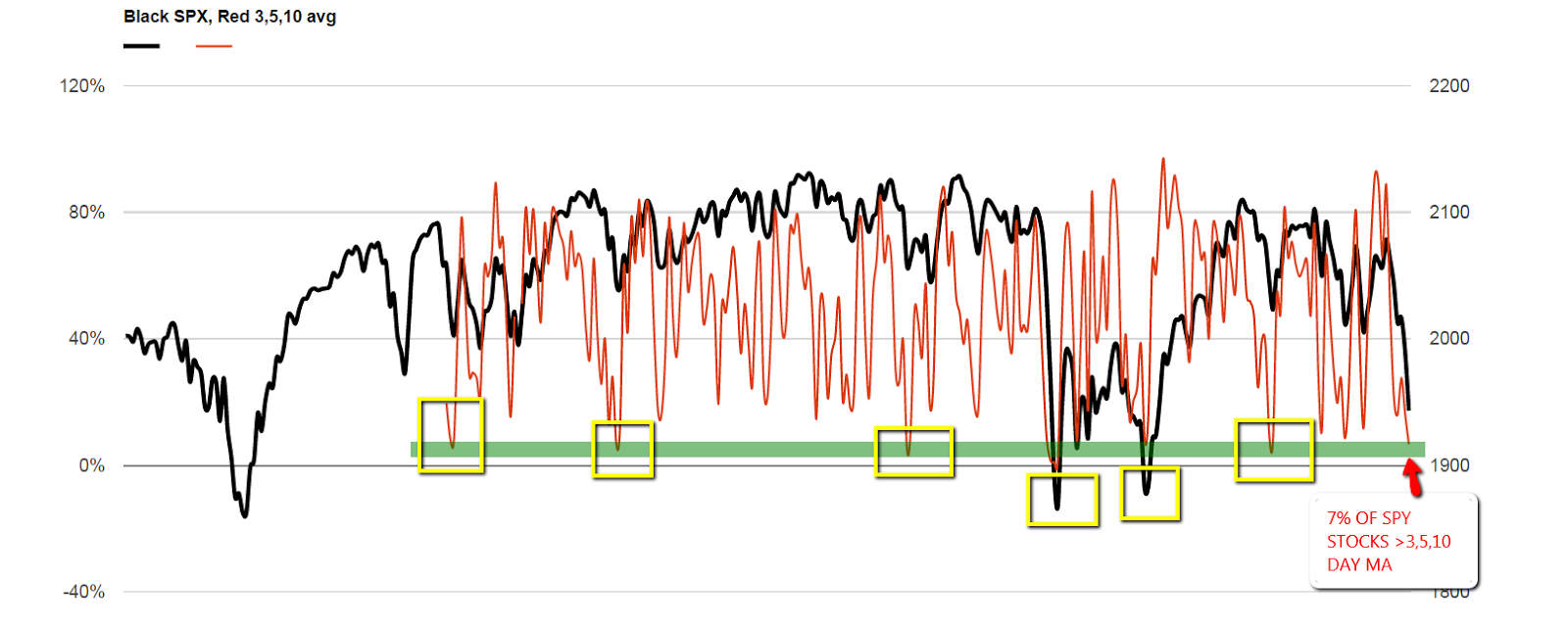

The percent of S&P500 stocks above their respective 3,5 and 10-day moving average is singing the same tune.

I want to make something clear; these short-term breadth extremes normally are short-term positives that produce 3-5 days dead cat bounces. Then we usually get a retest of the price low, and that’s when might see some positive divergences that may lead to a sustain bounce.

4%, 13% breadth charts courtesy of Pradeep Bonde

Leave A Comment